Understanding Intentionally Defective Grantor Trusts with a Diagram

An Intentionally Defective Grantor Trust (IDGT) is a type of trust that is purposely designed to be “defective” for income tax purposes. This unique trust structure allows the grantor to transfer assets to the trust while still retaining certain powers and benefits, such as the ability to pay income taxes on the trust’s income. This intentional “defect” enables the trust to be treated as a separate entity for estate tax purposes, while still being disregarded for income tax purposes.

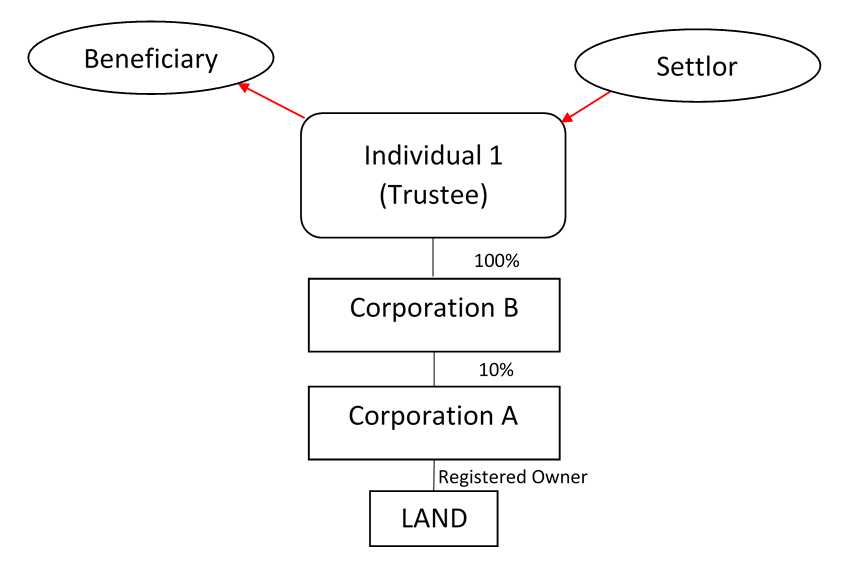

One way to understand the concept of an IDGT is through a diagram. Picture a triangle with three points: the grantor, the trust, and the beneficiaries. The grantor is the person who creates and funds the trust, transferring assets into it. The trust then holds and manages these assets for the benefit of the beneficiaries. However, unlike traditional trusts, the grantor in an IDGT is allowed to retain certain control over the trust.

At the top of the triangle, the grantor has the power to remove or replace the trustee, ensuring that the trust is managed in a way that aligns with their wishes. This control gives them the ability to oversee how the trust assets are invested and distributed, providing a level of flexibility and security. Additionally, the grantor can also retain the power to make minor changes to the trust, such as adding or removing beneficiaries.

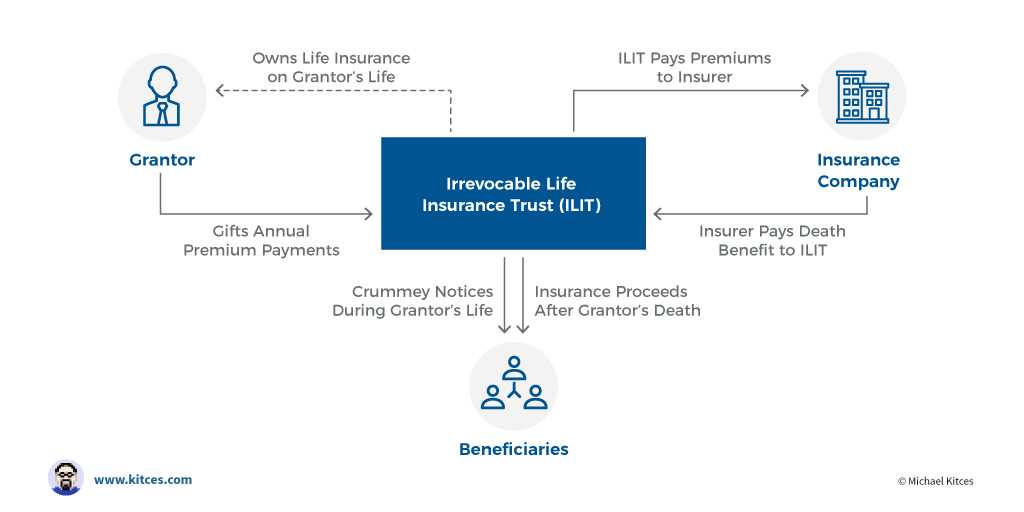

Intentionally Defective Grantor Trust Diagram

An intentionally defective grantor trust (IDGT) is a powerful estate planning tool that allows individuals to transfer assets out of their estate while still maintaining control over them. This type of trust is “defective” for income tax purposes, meaning that the grantor, or person creating the trust, is responsible for paying taxes on the income generated by the trust assets.

The diagram below illustrates the basic structure of an intentionally defective grantor trust:

- Grantor: The individual who creates the IDGT and funds it with assets.

- Trust: The legal entity that holds and manages the trust assets.

- Trustee: The person or entity responsible for managing the trust assets and carrying out the terms of the trust.

- Beneficiaries: The individuals or organizations who will receive the trust assets or income from the trust.

- Initial Funding: The grantor transfers assets to the trust, which are then owned by the trust and no longer part of the grantor’s estate.

- Income Tax Treatment: The trust is designed to be “defective” for income tax purposes, meaning that the grantor, not the trust, is responsible for paying taxes on the income generated by the trust assets. This allows the trust assets to grow without being diminished by income tax payments.

- Control and Benefits: Despite transferring assets to the trust, the grantor can still maintain control over the assets and continue to benefit from them during their lifetime. This can include receiving income generated by the trust, using the trust assets, or even retaining the power to make changes to the trust.

- Transfer of Assets: Upon the grantor’s death, the trust assets can be distributed to the beneficiaries according to the terms of the trust. This can help to minimize estate taxes and ensure that the assets are transferred to the intended recipients.

An intentionally defective grantor trust can be a complex estate planning tool, but when used correctly, it can provide significant tax advantages and flexibility for individuals looking to transfer assets out of their estate while still maintaining control over them.

Definition and Purpose of an Intentionally Defective Grantor Trust

An Intentionally Defective Grantor Trust (IDGT) is a type of trust that is intentionally designed to be defective for income tax purposes but still effective for estate planning purposes. The term “defective” refers to the fact that the trust is disregarded for income tax purposes, meaning that the grantor is still responsible for paying the income tax on the trust’s earnings, even though the trust assets are outside of the grantor’s estate for estate tax purposes.

The purpose of an IDGT is to transfer assets out of an individual’s estate while still allowing the individual to maintain control over the assets and receive the income generated by the trust. By paying the income tax on the trust’s earnings, the grantor is effectively making additional gifts to the trust without incurring gift tax liability. This can be a useful strategy for individuals who have a large estate that may be subject to estate taxes and want to minimize the tax impact on their beneficiaries.

One of the key benefits of an IDGT is that it allows for tax-free growth of the trust assets. Because the grantor is responsible for paying the income tax, the trust assets can grow without being reduced by income taxes. This can result in a significant increase in the value of the trust assets over time, providing a greater benefit to the beneficiaries. Additionally, since the trust is disregarded for income tax purposes, the grantor can sell assets to the trust without recognizing capital gains, allowing for tax-efficient asset transfers.

In conclusion, an Intentionally Defective Grantor Trust is a powerful estate planning tool that allows individuals to transfer assets out of their estate while still retaining control and receiving income from the trust. By leveraging the tax benefits of an IDGT, individuals can minimize the impact of estate taxes and maximize the value of their assets for future generations.

Benefits and Drawbacks of an Intentionally Defective Grantor Trust

Intentionally Defective Grantor Trusts (IDGTs) are a popular strategy used in estate planning to achieve various financial goals. While this type of trust offers several benefits, it also comes with certain drawbacks that need to be considered.

Benefits of an Intentionally Defective Grantor Trust:

- Income tax advantages: One of the main benefits of an IDGT is the ability to transfer assets to the trust while still being responsible for paying income taxes on the trust’s income. This allows the assets to grow outside of the estate while reducing the grantor’s taxable estate.

- Estate tax planning: By removing assets from the grantor’s estate, an IDGT can help reduce estate taxes. Since the trust is “defective” for income tax purposes, any income or appreciation generated by the trust is not included in the grantor’s estate for estate tax purposes.

- Control and flexibility: The grantor can retain control over the trust assets by acting as the trustee, making investment decisions, and determining when and how distributions are made. This provides flexibility in managing and distributing the assets according to the grantor’s wishes.

- Asset protection: Assets transferred to an IDGT are typically protected from creditors, providing an additional layer of asset protection for the grantor and their beneficiaries.

Drawbacks of an Intentionally Defective Grantor Trust:

- Irrevocable nature: Once assets are transferred to an IDGT, they generally cannot be revoked or removed from the trust without potentially triggering adverse tax consequences. This lack of flexibility may not be suitable for individuals who anticipate needing access to the transferred assets in the future.

- Complexity and administrative burden: Establishing and maintaining an IDGT can be complex and require ongoing administrative tasks. This may involve additional costs and professional assistance to ensure compliance with tax and legal requirements.

- Potential loss of step-up in basis: Assets held in an IDGT do not receive a step-up in basis upon the grantor’s death. This means that beneficiaries may be subject to capital gains tax if they sell the assets in the future.

Overall, an Intentionally Defective Grantor Trust can be a powerful tool for estate planning, providing income tax advantages, estate tax planning opportunities, and asset protection. However, it is essential to carefully consider the drawbacks and consult with professionals to determine if this strategy aligns with your specific financial goals and circumstances.

Setting Up an Intentionally Defective Grantor Trust: A Summary

Establishing an intentionally defective grantor trust (IDGT) can be a powerful tool for estate planning and wealth transfer. By intentionally making the trust “defective” for tax purposes, the grantor can benefit from certain tax advantages while still maintaining control over the assets. Here’s a summary of the steps involved in setting up an IDGT:

- Choose the trust’s assets: The grantor must select the assets that will be transferred to the IDGT. These assets can include cash, real estate, stocks, or other investments.

- Create the trust agreement: The grantor will need to work with an attorney to draft a trust agreement that meets the specific requirements of an IDGT. The agreement should include details about the trust’s purpose, beneficiaries, and trustee.

- Transfer assets to the trust: Once the trust agreement is completed, the grantor will transfer ownership of the selected assets to the IDGT. This can be done through various methods, such as gifting or selling the assets to the trust.

- Assign the grantor’s responsibilities and powers: To make the trust intentionally defective, the grantor should retain certain powers and responsibilities over the trust. This can include the ability to substitute assets, control investments, and make distributions.

- Consider tax implications: While the IDGT is intentionally defective for income tax purposes, it is still subject to certain estate and gift tax rules. The grantor should work with a tax professional to understand the potential tax consequences of establishing and funding the trust.

- Monitor and manage the trust: Once the IDGT is established, the grantor or a designated trustee will need to oversee the trust’s operations. This includes managing the trust’s investments, filing any required tax returns, and making distributions to beneficiaries as outlined in the trust agreement.

Overall, setting up an intentionally defective grantor trust requires careful planning and consideration of the grantor’s goals and financial situation. It is important to work with experienced professionals, such as attorneys and tax advisors, to ensure the trust is structured correctly and aligns with the grantor’s estate planning objectives.